Orange County Newsletter - June 2023

Note: You can find the charts & graphs for the Big Story at the end of the following section.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

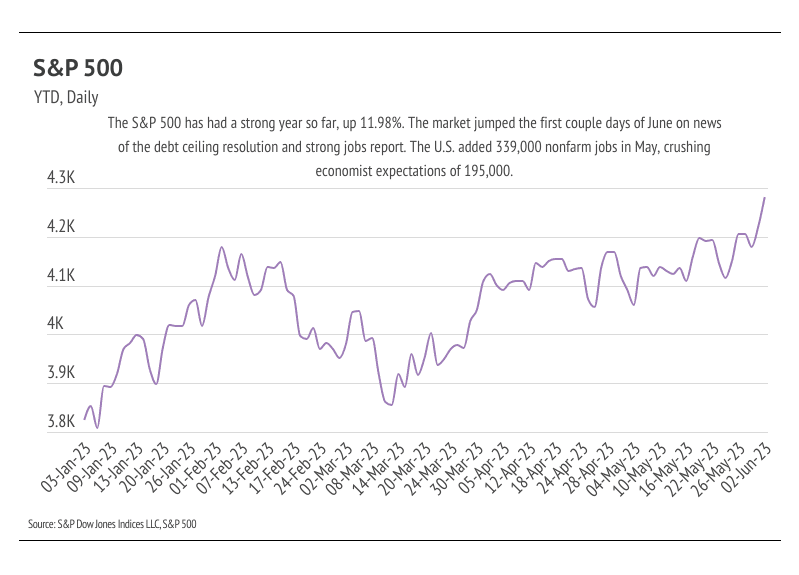

We did it, gang! We made it through another debt ceiling crisis! The United States paid its bills in full and on time, avoiding default and a global economic catastrophe with two days to spare. This self-inflicted wound would have had far-reaching negative economic consequences in the near and long term, including far higher mortgage rates. Financial markets were mostly unbothered despite the fact that this Congress seems to be the most amenable to default. The 10-year Treasury yield rose a modest 0.4% in May, which translated to a 0.4% increase in the average 30-year mortgage rate. The S&P 500, which tracks the stock of the 500 largest publicly traded U.S. companies, reached a high for the year at the beginning of June, up 12% year to date. To be fair, a debt ceiling resolution that didn’t totally destroy the U.S.’s global standing was the most probable scenario. Now that the debt ceiling has been lifted until 2025, we turn our sights back to the Fed and interest rates.

During their last meeting, the Fed forecasted a potential pause in rate hikes after three sizable regional bank failures this year, but recent jobs data may swing them back toward a 0.25% increase. Increasing mortgage rates have primarily driven the housing market slowdown we’ve experienced over the past 12 months. Higher rates affect the housing market so strongly because housing is typically financed. Potential buyers have struggled with mortgage rate volatility over the past 18 months, as the average 30-year mortgage rate went from historic lows in 2021 (~3%) to a 20-year high (~7%) in November 2022. Luckily, rates contracted but have remained around 6.5%. Because home prices nationally haven’t contracted substantially from their all-time highs, small rate changes can make a huge difference in the cost of financing. The average 30-year rate hit a 2023 high at the start of June. However, we still expect rates to stay within the 6-7% band this year. At this point, continued rate hikes tell us more about the length of time rates will stay high, since the Fed tends to move in smaller steps over time. This means that, for every step up, there will need to be a step down, which will prolong the process of returning to lower mortgage rates.

The Fed has a tricky decision regarding future rate hikes. The broad labor market has shown its strength and seeming immunity to rate hikes. The monthly increase in employment from the U.S. Bureau and Labor Statistics has beat Wall Street estimates for the 14th month in a row. In May alone, 339,000 jobs were created, crushing the expected 195,000 jobs. At the same time, however, unemployment rose from 3.4% to 3.7% from April to May. Additionally, the first-quarter 2023 GDP data was revised up from 1.1% to 1.3% quarter over quarter. With this mix of data, we’re expecting a rate hike pause at the June meeting, but a hike again in July.

The housing market is in an interesting spot, where the economy is too good to lower rates but homes have become too expensive for potential buyers. Fewer sellers and buyers are in the market, so sales are unlikely to grow meaningfully this year.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. In general, higher-priced regions (the West and Northeast) have been hit harder by mortgage rate hikes than less expensive markets (the South and Midwest) because of the absolute dollar cost of the rate hikes and the limited ability to build new homes. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Quick Take:

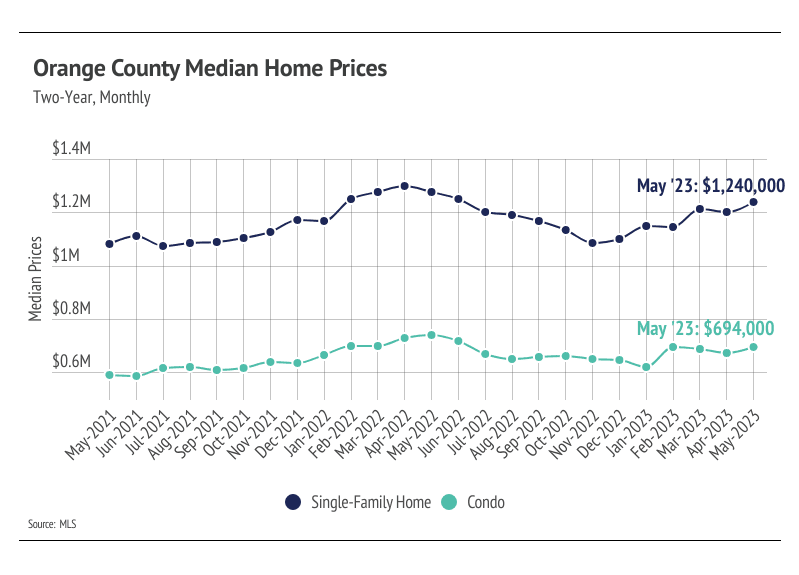

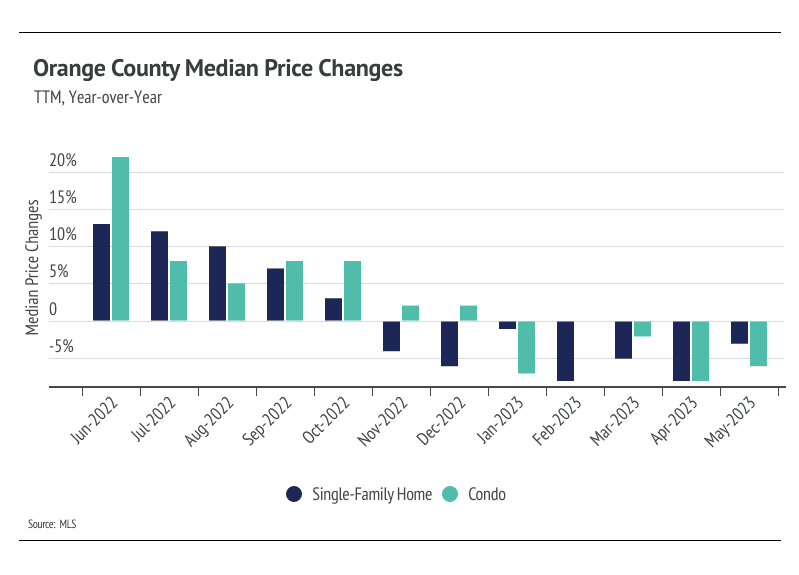

The median single-family home price rose 12.7% year to date, landing only 4.6% below the record high hit last year. Condo prices aren’t far behind, 6.2% below last year’s all-time high.

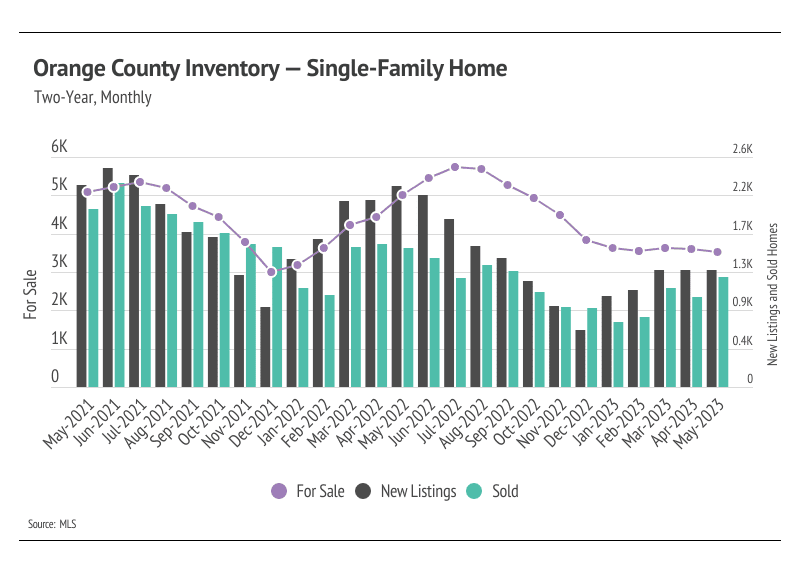

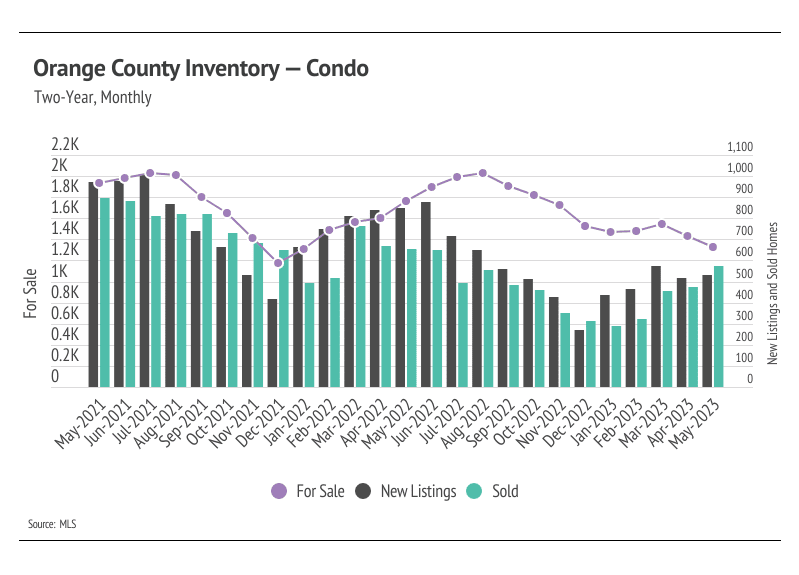

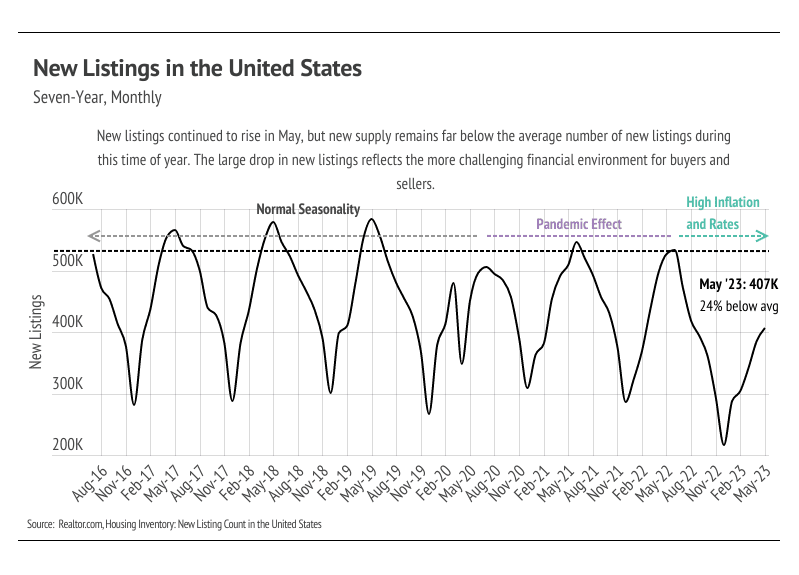

Active listings in Orange County fell in May, continuing a 10-month trend, as sales increased and fewer than usual new listings came to market.

Months of Supply Inventory has declined significantly in 2023, homes are selling more quickly, and sellers are receiving a greater percentage of asking price, all of which highlight an increasingly competitive environment for buyers.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

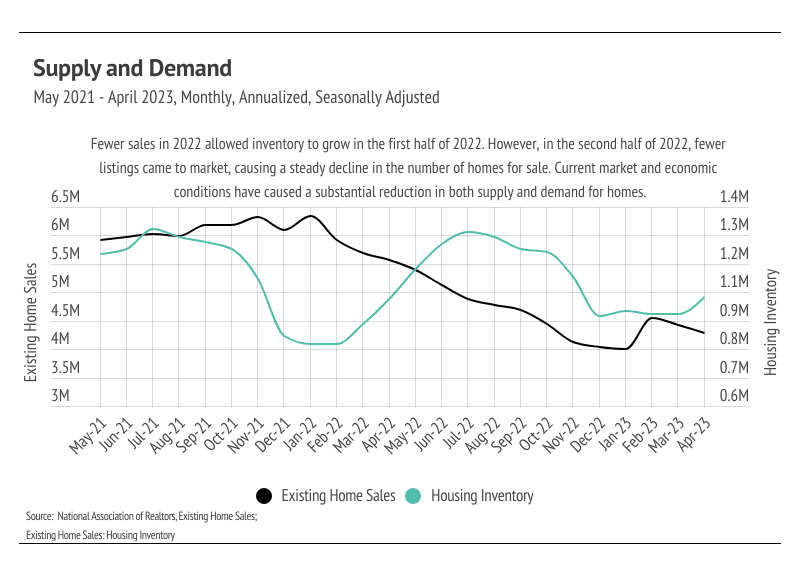

Increasing demand and low inventory are once again driving the rapid home price appreciation that Orange County has experienced this year. Last year, single-family home prices peaked in April, and condo prices peaked in May, as buyers rushed to lock in a lower mortgage rate. The Fed announced rate hikes at the end of 2021 that would swiftly affect rates in 2022. The average 30-year mortgage rate rose 2% in the first four months of 2022, crossing 5% for the first time since 2011. That 2% jump caused the monthly cost of financing to increase 27%, so buyers rightly rushed to the market. As rates rose higher, the market cooled and home prices fell in large part to accommodate the higher cost of a mortgage. Both supply and demand were lower than normal in the second half of 2022. However, in 2023, demand started to rise again despite elevated mortgage rates, but it wasn’t met with the typical number of new listings.

This year, the number of new listings has been significantly lower than usual compared to sales growth. Typically, inventory grows in the first half of the year as new listings significantly outpace sales. At this point, inventory levels can’t make up for the declines in the first five months of 2023, keeping supply of homes and, in turn, sales depressed for the rest of the year. As demand increases through the summer months, competition among buyers will climb with it, raising home prices. Single-family home and condo prices are near their record highs, and if active listings continue to decline, we could easily see home prices reach new record highs in July or August.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

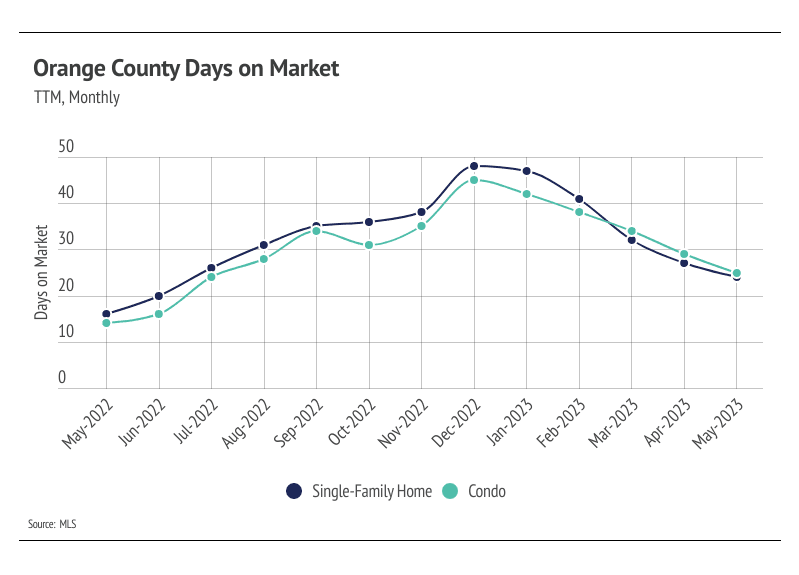

Single-family home and condo inventory has been declining for the past 10 months. Sales and new listings grew from April to May, but sales far outpaced homes coming to the market. Additionally, inventory, sales, and new listings are all significantly lower than last year. The number of home sales is, in part, a function of the number of active listings and new listings coming to market. Even though new listings are at a depressed level, they are increasing, positively affecting sales. Currently, inventory is so low relative to demand that far more new listings could come to the market. Potential sellers who have fully paid off their property are in a particularly good position if they don’t have to finance their next property after the sale of their home. Since January, sales jumped 77% while new listings rose 30%.

As buyer competition has ramped up and sellers are gaining negotiating power, sellers are receiving more of their listed price. In January 2023, the average seller received 93% of list price compared to 99% of list in May. Inventory will almost certainly remain depressed for the rest of the year, and the market will likely only get more competitive in the summer months.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI dropped over the past four months for both single-family homes and condos, meaning the market favors sellers. The sharp drop in MSI occurred due to the higher proportion of sales relative to active listings and less time on the market.

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Explore the places, neighborhoods, and people that make the communities we serve special. We’ve highlighted important market data, school information, and neighborhood highlights to help you find your new home.

Stay up to date on the latest real estate trends.

Seasonal Inventory Declines and Price Stabilization?

July 2024

Coastal Splendor: Explore Exquisite Waterfront Properties in Orange County Orange County's coastal charm is epitomized by its stunning waterfront properties, each off… Read more

The Role of Schools in Orange County Home Values: Unraveling the Correlation Between Education and Property Investment In the intricate tapestry of real estate, vario… Read more

Historic Homes in Orange County: A Journey Through Time Embark on a captivating journey through Orange County's rich history as we explore the charm and elegance of i… Read more

Happy Wednesday to you all and sorry to get this to you about a week later than normal. Spring break with the kids, busy listings, and life got in the way. So without … Read more

Well its the begining of "listing season" but where are the homes? Long story short, they are coming but its probably going to be a bit. The market is starving for inv… Read more

The 9 Best Neighborhoods to Live in Orange County