July 2024 Orange County Real Estate Market Update

Explore the places, neighborhoods, and people that make the communities we serve special. We’ve highlighted important market data, school information, and neighborhood highlights to help you find your new home.

Stay up to date on the latest real estate trends.

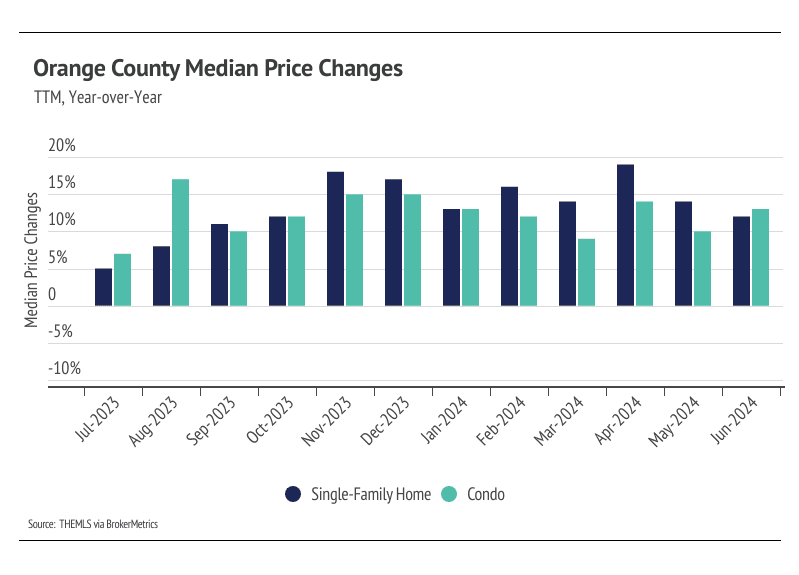

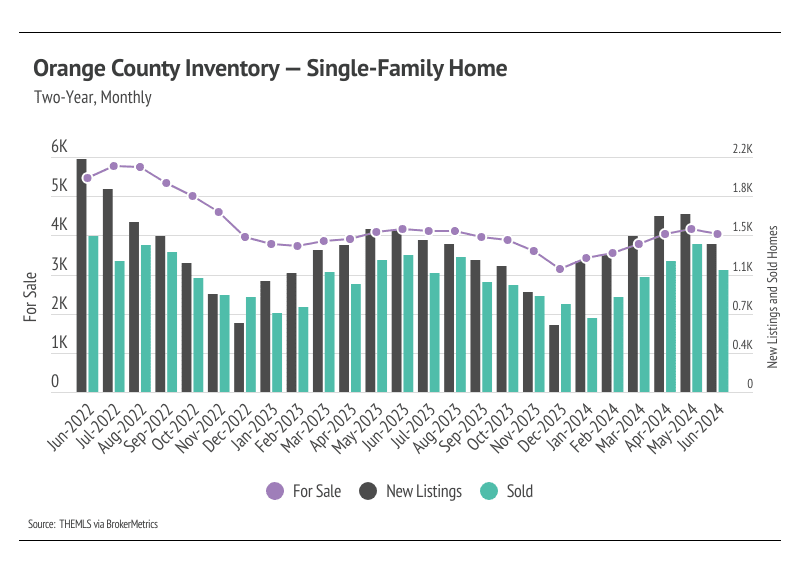

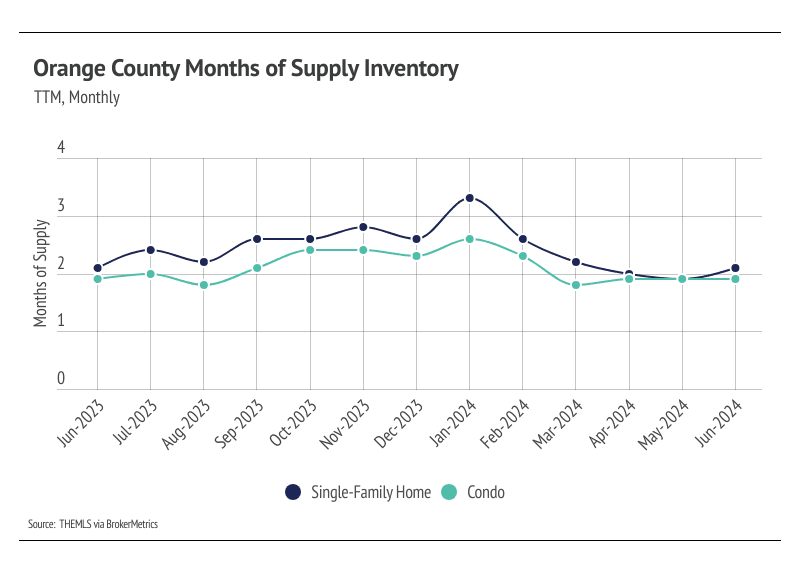

Seasonal Inventory Declines and Price Stabilization?

July 2024

Coastal Splendor: Explore Exquisite Waterfront Properties in Orange County Orange County's coastal charm is epitomized by its stunning waterfront properties, each off… Read more

The Role of Schools in Orange County Home Values: Unraveling the Correlation Between Education and Property Investment In the intricate tapestry of real estate, vario… Read more

Historic Homes in Orange County: A Journey Through Time Embark on a captivating journey through Orange County's rich history as we explore the charm and elegance of i… Read more

Happy Wednesday to you all and sorry to get this to you about a week later than normal. Spring break with the kids, busy listings, and life got in the way. So without … Read more

Well its the begining of "listing season" but where are the homes? Long story short, they are coming but its probably going to be a bit. The market is starving for inv… Read more

The 9 Best Neighborhoods to Live in Orange County